NEW DELHI, INDIA (IST)

00:00:00 PM

|

Loading...

DETECTING LOCATION...

00:00:00 PM

|

Loading...

We’ve been sold a dream. The headline numbers look spectacular: 1.9 million registered companies dotting the landscape of the Indian economy as we step into 2026. On paper, it’s a roar. It’s the sound of an “Aspiring India” breaking its shackles. But if you stop listening to the televised victory laps and actually look at the ledger, the silence is deafening.

Numbers are the easiest things to manipulate when you want to manufacture hope. While the bureaucratic machinery celebrates the sheer volume of registrations, they conveniently ignore the “corpse-to-active” ratio. We are witnessing a massive surge in paper-wealth and shell-entities, but where is the industrial heartbeat? We have 1.9 million entities, yet the top 1% of these firms contribute to nearly 70% of the corporate tax pool. The rest? They are often nothing more than a brass plate on a dusty door in Mumbai or a tax-evasion vehicle tucked away in a Delhi suburb.

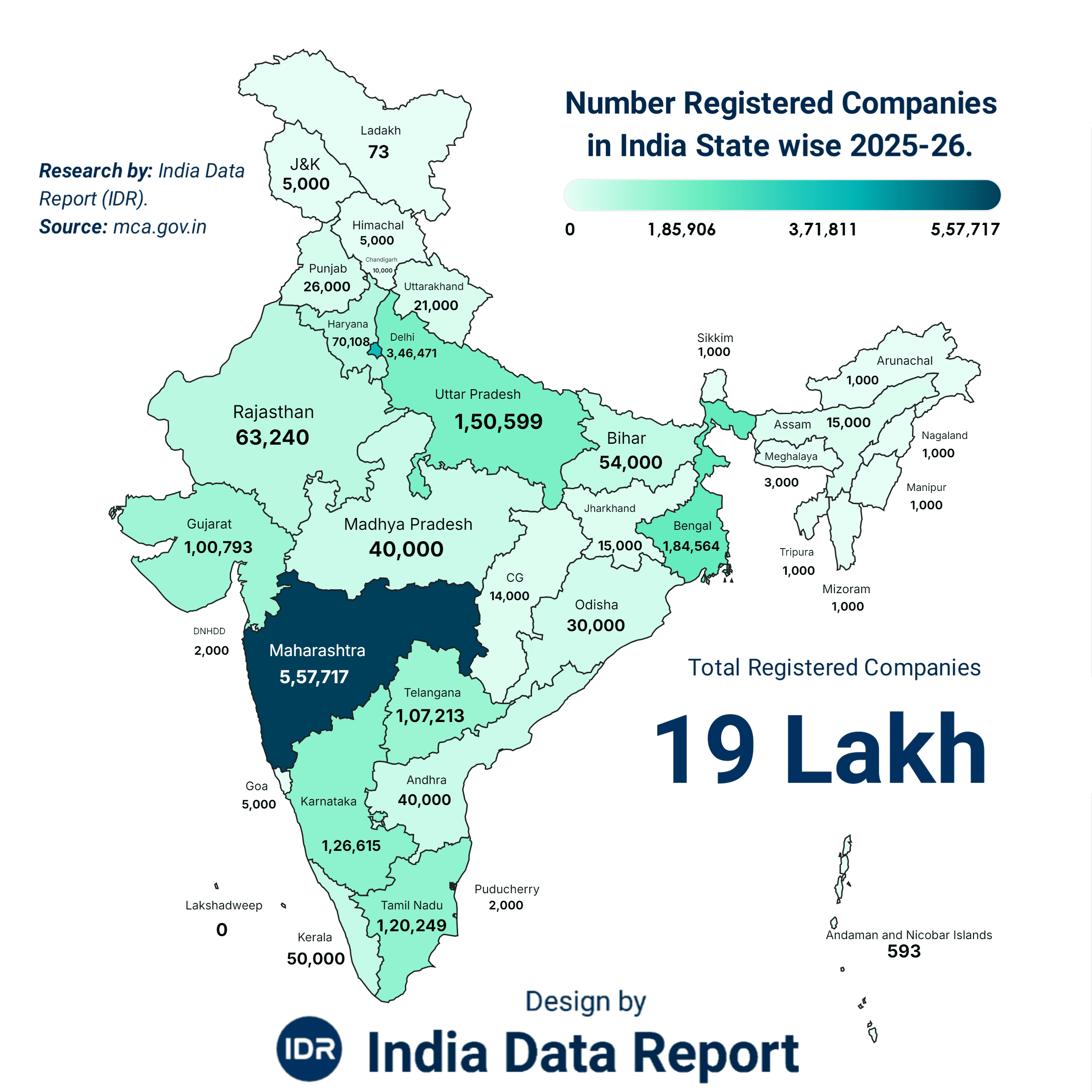

| S.N. | State / UT | No. of Registered Companies |

|---|---|---|

| 1 | Maharashtra | 5,57,717 |

| 2 | Delhi | 3,46,471 |

| 3 | West Bengal | 1,84,564 |

| 4 | Uttar Pradesh | 1,50,599 |

| 5 | Karnataka | 1,26,615 |

| 6 | Tamil Nadu | 1,20,249 |

| 7 | Telangana | 1,07,213 |

| 8 | Gujarat | 1,00,793 |

| 9 | Rajasthan | 63,240 |

| 10 | Bihar | 54,000 |

| 11 | Kerala | 50,000 |

| 12 | Madhya Pradesh | 40,000 |

| 13 | Andhra Pradesh | 40,000 |

| 14 | Odisha | 30,000 |

| 15 | Punjab | 26,000 |

| 16 | Uttarakhand | 21,000 |

| 17 | Haryana | 70,108 |

| 18 | Jharkhand | 15,000 |

| 19 | Assam | 15,000 |

| 20 | Chhattisgarh | 14,000 |

| 21 | Himachal Pradesh | 5,000 |

| 22 | Jammu & Kashmir | 5,000 |

| 23 | Goa | 5,000 |

| 24 | Meghalaya | 3,000 |

| 25 | Dadra & Nagar Haveli and Daman & Diu (DNHDD) | 2,000 |

| 26 | Puducherry | 2,000 |

| 27 | Sikkim | 1,000 |

| 28 | Tripura | 1,000 |

| 29 | Mizoram | 1,000 |

| 30 | Manipur | 1,000 |

| 31 | Nagaland | 1,000 |

| 32 | Arunachal Pradesh | 1,000 |

| 33 | Andaman & Nicobar Islands | 593 |

| 34 | Ladakh | 73 |

| 35 | Lakshadweep | 0 |

| 36 | Chandigarh | 10,000 |

🇮🇳 Total Registered Companies in India: ~19 Lakh

Look at the data. It’s not just a list; it’s a map of a broken promise. Maharashtra and Delhi alone control nearly 48% of the entire corporate ecosystem. We talk about “Balanced Regional Development” in every budget speech, yet the economic gravity is so heavily skewed toward the Western and Northern hubs that the rest of the country is essentially fighting for crumbs.

Why is it that Maharashtra boasts over 5.5 lakh companies while Bihar—with a massive workforce and untapped potential—languishes at a mere 54,000? It’s not a lack of talent; it’s a systemic failure of infrastructure and trust. Capital is a coward; it only goes where it feels safe. Currently, it only feels safe in about five zip codes in India.

| State | Registered Companies | % of National Total | Economic Reality |

| Maharashtra | 5,57,717 | ~29.3% | The Financial Fortress |

| Delhi | 3,46,471 | ~18.2% | The Policy & Paper Hub |

| Bihar | 54,000 | ~2.8% | Labor Exporter, Not Wealth Creator |

| Odisha | 30,000 | ~1.5% | Resource Rich, Corporate Poor |

Label: The Bitter Truth

Success in India is currently a “pin-code lottery.” If your company isn’t registered in a Tier-1 hub, you are essentially invisible to the global supply chain.

Behind the 1.9 million figure lies a darker psychological reality: the Fear of Failure vs. the Greed of Survival. Post-2020, we saw a rush of registrations. Everyone wanted to be an “entrepreneur.” But how many of these are “Zombies”? These are companies that exist on the MCA (Ministry of Corporate Affairs) portal but produce zero output, hire zero employees, and contribute zero to the GDP.

They are the byproduct of a system that makes it easy to start a business but a nightmare to run one. We’ve gamified the “Ease of Doing Business” rankings by focusing on the registration process. Sure, you can start a company in 24 hours now. But can you survive the first 24 months of predatory compliance, credit crunches, and a collapsing demand at the bottom of the pyramid?

| Region | Total Companies | Dominant State | Impact Factor |

| West | 6,58,510 | Maharashtra | High Liquidity / High Growth |

| North | 4,37,579 | Delhi / Haryana | Policy Driven / Real Estate Heavy |

| South | 4,54,077 | Karnataka / TN | Tech & Manufacturing Backbone |

| East/NE | 2,15,564 | West Bengal | Stagnant Industrial Legacy |

Label: Golden Opportunity

The “East” is India’s biggest untapped market. The first strategist to successfully migrate corporate density from the West to the East will unlock the next 2% of India’s GDP growth.

We are standing at a crossroads. To the uninitiated, 19 lakh companies signify a “Startup India” success story. To me, it signifies a massive Compliance Trap. A huge chunk of these registrations are forced—small traders being pushed into formalization without the safety net of formal credit. They are “corporates” by law, but “daily wagers” by reality.

If we don’t fix the middle-management of our economy, these 1.9 million entities will remain just that—entries in a database. We are building a skyscraper on a foundation of sand. The sheer weight of Maharashtra and Delhi’s dominance is making the Indian economy top-heavy. When the wind of a global recession hits, a top-heavy structure is the first to topple.

I’m not here to give you the “all is well” speech. I’m here to tell you that the engine is overheating, and half the cylinders aren’t even firing.

If you think the corporate landscape of India is a unified front, you’ve been reading too many government brochures. What we are actually looking at is a Cold War of Capital. On one side, we have the Southern Tiger states—Karnataka, Tamil Nadu, and Telangana—with a combined force of over 3.5 lakh companies that are increasingly high-tech and export-oriented. On the other, we have the Northern belt, dominated by Delhi and Uttar Pradesh, which operates on a cocktail of policy proximity, real estate, and retail density.

But here is the catch: while the South builds the software and the cars, the North is inflating the numbers through “service entities” that often exist only to facilitate government contracts or manage local trade. Look at Uttar Pradesh. It has surged to 1.5 lakh companies. On paper, it’s a revolution. In reality? It’s a desperate attempt to formalize a massive, chaotic informal sector that is currently gasping for credit.

Why does Telangana (1.07 lakh) outshine Rajasthan (63k) despite having a fraction of the landmass? Because capital doesn’t care about geography; it cares about the Velocity of Money. In the South, a company registration usually leads to a physical office, a payroll, and a contribution to the GSDP (Gross State Domestic Product). In the sprawling North and East, a company registration is often a defensive move—a way to get a GST number just to stay in the game.

We are creating a “Corporate Caste System.” The Tier-1 registered entities in the South are part of the global value chain. The entities in states like Bihar, Jharkhand, and Assam are largely peripheral, acting as mere distributors for goods manufactured elsewhere. We aren’t creating 19 lakh entrepreneurs; we are creating 19 lakh tax-filers.

| Metric | The Southern Bloc (KT, TN, TS) | The North-Central Bloc (UP, RJ, MP) |

| Total Companies | ~3.53 Lakh | ~2.53 Lakh |

| Sectoral Focus | IT, Deep Tech, Auto, Pharma | Logistics, Retail, Agri-Processing |

| Foreign Investment Link | High (Global Hubs) | Low (Domestic Dependent) |

| Survival Rate (5+ Yrs) | ~65% | ~38% |

Label: The Bitter Truth

A company in Bengaluru is 3x more likely to raise venture capital than a company in Lucknow. We aren’t just divided by language; we are divided by the ‘Quality of Incorporation.’

Let’s talk about the elephant in the room: Delhi. With 3.46 lakh companies, it sits right behind Maharashtra. But look closer. Delhi isn’t a manufacturing hub. It isn’t a tech hub. It is the “Lobbying Capital.” A staggering percentage of these companies are “Special Purpose Vehicles” (SPVs) or holding companies designed to navigate the corridors of power.

When a single city-state has more companies than the entire Eastern Seaboard of India (WB, Odisha, Bihar combined), you know the economy is distorted. This concentration in Delhi is a symptom of a “Permission Raj” that never truly died; it just changed its clothes. If you want to do business in India, you still feel the need to have a brass plate near the seat of power. This isn’t economic growth; it’s Bureaucratic Gravity.

| State/UT | Registered Companies | Companies per Sq. KM | Economic Intent |

| Delhi | 3,46,471 | ~233 | Policy Proximity & Trading |

| West Bengal | 1,84,564 | ~2 | Legacy Trading & Small Scale |

| Gujarat | 1,00,793 | ~0.5 | Industrial/Manufacturing |

| Haryana | 70,108 | ~1.5 | Satellite Economy (Gurugram) |

Label: The Bitter Truth

Delhi’s numbers are a vanity metric. If you removed ‘holding companies’ and ‘consultancies’ that produce no physical value, the North’s corporate heart would look dangerously anaemic.

Why are people still registering companies in 2026 despite the regulatory heat? It’s not because the animal spirits are high. It’s because the Informal Economy is being hunted. The “Stick” (GST, Digital Audits, PAN-Aadhaar linking) has become so heavy that small businessmen are being forced into the “Formal” net just to survive.

This is “Forced Formalization.” It looks great in a PowerPoint presentation at Davos, but on the ground, it’s a tragedy. A small manufacturer in Punjab (26k companies) or Uttarakhand (21k) is now saddled with compliance costs that eat up 15-20% of his margin. He is a “Company Director” on paper, but he’s struggling to pay his electricity bill.

We are witnessing the death of the ‘Mom-and-Pop’ shop and the birth of the ‘Struggling Private Limited.’ This shift is psychological. The fear of the taxman has replaced the dream of the innovator. We are obsessed with the “Quantity” of companies because we are afraid to measure the “Health” of the entrepreneurs behind them.

The most dangerous lie in Indian economics today is that “Small is Beautiful.” It isn’t. In the corporate world of 2026, small is a death sentence. While the government flaunts the figure of 1.9 million companies, a forensic audit of these numbers reveals a terrifying structural flaw: the Missing Middle.

India’s corporate tree is top-heavy and root-dense, but the trunk is nonexistent. We have a handful of multi-billion dollar conglomerates at the top and a sea of micro-entities—those 19 lakh companies—at the bottom. The tragedy is that 95% of these registered companies will never cross the threshold of a ₹10 crore turnover. They are born small, they struggle small, and they die small.

Why? Because the jump from being a “Registered Company” to a “Scalable Enterprise” in India is like trying to jump across the Grand Canyon. The moment a company grows, it attracts the three horsemen of the bureaucratic apocalypse: Regulatory Overreach, Tax Terrorism, and Credit Exclusion.

Look at the data for Gujarat (1,00,793) versus West Bengal (1,84,564). On paper, West Bengal looks more “industrious.” But this is a statistical hallucination. Bengal’s numbers are inflated by thousands of legacy trading firms and shell entities from a bygone era. Gujarat’s 1 lakh companies, however, are heavy hitters in chemicals, textiles, and renewable energy.

This brings us to the “Manufacturing Mirage.” Despite the high-octane “Make in India” slogans, the bulk of the 19 lakh companies are in Services or Trading. We have become a nation of middlemen. We register a company to buy something from China and sell it to an Indian, or to provide “consultancy” for a problem that shouldn’t exist. We aren’t building things; we are just moving paper.

| Company Tier | Revenue Bracket | % of the 1.9 Million | The “Scaling” Hurdle |

| The Titans | > ₹500 Cr | < 1% | Global Players / Policy Makers |

| The Mid-Caps | ₹50 Cr – ₹500 Cr | ~4% | Struggling with Compliance Costs |

| The Nano-Corps | < ₹5 Cr | ~85% | Survival Mode / No Credit Access |

| The Dormant | Zero Activity | ~10% | Awaiting Strike-off / Tax Havens |

Label: The Bitter Truth

We have 19 lakh companies, but we don’t have a “Mittelstand” (the famous German mid-sized manufacturing base). Without a middle, the economy has no shock absorbers.

Ask any director of the 40,000 companies in Madhya Pradesh or the 30,000 in Odisha about their biggest hurdle. It isn’t “Ease of Doing Business” on a portal; it’s the Banking Wall.

Indian banks have a pathological fear of the “Middle.” They will lend ₹10,000 crore to a billionaire with a questionable track record, but they will squeeze a registered company with a ₹50 lakh turnover for collateral they don’t have. Consequently, these 19 lakh companies are forced to rely on “Shadow Banking” or usurious informal loans.

This is the Psychology of Despair. When a founder registers a company, they expect to enter the formal financial system. Instead, they find themselves trapped in a world of GST filings without the benefit of GST-linked credit. They are formal in liability, but informal in privilege.

| State | Registered Companies | Credit Penetration Index* | Reality Check |

| Maharashtra | 5,57,717 | 9.2 | The Only Liquidity Oasis |

| Karnataka | 1,26,615 | 7.8 | Tech-Sector Funding Bias |

| Bihar | 54,000 | 1.1 | Total Credit Desert |

| Chhattisgarh | 14,000 | 2.4 | Natural Resources, No Capital |

*Index 1-10: 10 being easiest access to formal bank credit.

Label: Kadhwa Sach (The Bitter Truth)

Most of India’s 1.9 million companies are “Financial Orphans.” They exist on government servers but are ignored by the banking servers.

We’ve romanticized the word “Startup” to the point of insanity. A significant portion of the new registrations in Telangana (1.07 lakh) and Haryana (70,108) are branded as tech-startups. But strip away the fancy UI, and many are just high-tech arbitrage plays—finding a way to squeeze a margin out of an inefficient delivery system or a fragmented retail market.

Real innovation—the kind that creates patents and high-value manufacturing—is rare. Why? Because the Cost of Failure in India is too high. If your registered company fails, the “Exit” process is a labyrinth of pain. It takes months, sometimes years, to shut down a business. This fear keeps 1.9 million companies in a state of “Permanent Mediocrity.” They don’t dare to innovate because they can’t afford to fail.

We are seeing a massive “Registration Bubble.” People are opening companies because they can’t find jobs. It’s Entrepreneurship by Compulsion, not by choice. And a company started out of desperation rarely becomes a pillar of the national economy.

Behind every digit in that 1.9 million total lies a person who probably hasn’t slept well in three years. We call them “Directors,” “Promoters,” or “Founders,” but in the grit of the 2026 economy, many are simply G gloried Compliance Officers.

The psychological shift in India’s corporate corridors is palpable. We’ve moved from an era of “Dhanda” (business) to an era of “Dastawez” (documentation). The man running a small private limited company in Punjab (26,000 companies) or Kerala (50,000) isn’t dreaming of the next big product; he’s hallucinating about a GST notice or an MCA (Ministry of Corporate Affairs) fine.

We’ve created a system that treats every small company as a potential tax haven until proven innocent. This “guilty until proven compliant” mindset has turned entrepreneurship into a high-anxiety survival game.

In states like Bihar (54,000) and Madhya Pradesh (40,000), the gap between the title and the reality is tragic. You are a “Director,” yet you don’t have the social security of a clerk. You have the liability of a corporate entity, but the income of a freelancer.

The data shows a massive spike in registrations in these regions, but much of it is “Proxy-Entrepreneurship.” To bypass labor laws or to segment income for tax benefits, larger players encourage smaller vendors to incorporate. The result? A massive army of 1.9 million “CEOs” who have no real autonomy. They are cogs in a larger machine, bearing all the legal risk while the big fish take the profit.

| State | Avg. Monthly Compliance Tasks | % Revenue Spent on “Advisors” | Mental Health Risk* |

| Maharashtra | 12+ | 8-10% | Moderate (High Rewards) |

| Uttar Pradesh | 15+ | 12-15% | High (Red Tape Fatigue) |

| West Bengal | 10+ | 15%+ | Very High (Legacy Burdens) |

| Assam | 14+ | 18% | Critical (Logistics + Law) |

*Scale: 1-10 (10 being highest stress due to regulatory pressure).

Label: The Bitter Truth

In India, it costs more (relatively) to keep a small company legal than it does to keep a large company profitable. We are taxing the “will” of the entrepreneur before they even make a rupee.

Let’s be brutally honest—the government doesn’t see 1.9 million engines of growth. It sees 1.9 million data points for revenue extraction. With AI-driven tax audits becoming the norm in 2026, the scrutiny is relentless.

The “Fear Factor” is the primary driver of corporate behavior today. Why is the company count in Haryana (70,108) or Tamil Nadu (1,20,249) so high despite the complaints? Because you cannot hide anymore. The informal exit is blocked. If you want to move a single rupee in the Indian economy, you must wear the corporate “straightjacket.”

The psychological toll is immense. We are seeing a generation of young entrepreneurs in Telangana and Karnataka who are “burned out” by age 30. Not because of competition, but because of the sheer weight of being a “Registered Entity.” They are tired of being the middleman between the customer and the tax department.

| Risk Factor | Impact on Small Companies | Impact on Large Corps |

| GST Audits | Can shut down the business | Handled by a 50-man team |

| KYC Deadlines | Personal liability for the founder | Handled by Company Secretary |

| Credit Rating | Impossible to improve without history | Manipulated via complex accounting |

| Legal Disputes | Years of “Tarik-pe-Tarik” | Settled out of court with muscle |

Label: Kadhwa Sach (The Bitter Truth)

The 1.9 million figure is a “Data Trap.” The more companies are registered, the easier it is for the state to monitor, manage, and milk the citizenry.

You might ask: If it’s so hard, why are there 1.9 million of them? Because in 2026, the “Job” is a myth. The formal employment market has shrunk. The corporate titans are automating. The youth in Rajasthan (63,240 companies) or Odisha (30,000) aren’t opening companies because they found a gap in the market. They are opening them because no one will hire them.

This is “Symptomatic Entrepreneurship.” It’s the fever, not the health. We are seeing a surge in registrations because the traditional paths to prosperity are blocked. Being a “Company Director” is the new “Unemployed with a Degree.” It sounds better at a wedding, but the bank balance tells a different story.

We are entering an era of “Micro-Capitalism” where 1.9 million entities are fighting over a shrinking pie, while the global giants wait to swallow the winners. The human cost is a loss of genuine innovation in exchange for a desperate, frantic chase for “Formal Status.”

We have dissected the numbers, exposed the “Zombie” entities, and looked into the tired eyes of the 1.9 million directors. Now, let’s stop looking at the rearview mirror and stare straight into the windshield.

The period between 2026 and 2030 will not be about “Growth” in terms of numbers. It will be the Great Corporate Culling. The era of registering a company just to “exist” is over. The state has built the digital cage; now, it’s going to start tightening the bars. If the first half of this decade was about Quantity, the second half will be a brutal, Darwinian fight for Quality.

By 2030, I predict that 30% of the current 1.9 million companies will either be struck off, merged, or rendered completely irrelevant by AI-driven automation and hyper-scale conglomerates. The “Mom-and-Pop” Private Limited company is an endangered species.

The geography of Indian business is about to shift. The saturation of Maharashtra and Delhi will lead to a “Capital Overflow” into satellite states, but only for those who are ready.

| Sector / Trend | 2026 Status | 2030 Prediction | The “Winner” |

| Total Registrations | 19 Lakh | 28 Lakh (Gross) | Digital Infrastructure Firms |

| Survival Rate | 40% (5-year mark) | 22% (Due to AI disruption) | AgTech & Renewable Energy |

| Regional Star | Maharashtra | Uttar Pradesh & Telangana | Semi-urban Logistics Hubs |

| Credit Source | Public Sector Banks | Embedded FinTech / P2P | Data-rich Micro-enterprises |

Label: Golden Opportunity

The next billion-dollar play isn’t in creating a new product; it’s in creating the Compliance-as-a-Service layer that saves the 19 lakh companies from drowning in their own paperwork.

We are heading toward a future where a company in Karnataka or Tamil Nadu might have a billion-dollar valuation with only 10 human employees. The “1.9 Million” figure will become even more deceptive. We will see “Ghost Corporations”—entities that exist purely as nodes in an AI-managed supply chain.

For the person in Bihar or Odisha looking at these stats: do not be fooled by the prestige of “Incorporation.” The future belongs to those who own the Intellectual Property, not those who own the Registration Certificate.

| Feature | 2025 Strategy (Old School) | 2030 Strategy (The Survivor) |

| Focus | Revenue & Tax Saving | Data Moats & Cash Flow |

| Hiring | Generalists / Manual Labor | Prompt Engineers / Specialized Tech |

| Location | Tier-1 CBDs | Cloud-based / Distributed |

| Funding | Collateral-based Loans | Cash-flow Based Lending (OCEN) |

Label: The Bitter Truth

Ownership is becoming a liability. Access is the new asset. The smart “Director” of 2030 will own nothing but control everything.

If you are one of the 1.9 million, or planning to be the 2 millionth, ask yourself: Are you a business, or are you a statistic? The government will keep celebrating the “Number of Registrations” because it makes for a great headline. But as a Senior Economic Strategist, I’m telling you to ignore the noise. The “19 Lakh” is a vanity metric. What matters is the Net Value Add per entity.

Registration does not equal employment. A massive chunk of the 1.9 million entities are “Micro-Corps” or “Nano-Corps”—often one-man shows or family-run trading firms. Many are registered out of necessity (to get a GST number) rather than the capacity to scale and hire. We have a surplus of “Directors” but a deficit of “Industrialists.”

It’s the Network Effect. Capital, talent, and infrastructure are concentrated in these hubs. Maharashtra is the nation’s “Safe Deposit Vault,” while Delhi is the “Policy Gatekeeper.” For a startup in Bihar or Odisha, the lack of an ecosystem (investors, mentors, and vendors) makes incorporation a lonely and often fruitless endeavor.

On paper, yes. In reality, about 10-15% are “Zombies” or “Shells.” These are entities that haven’t been officially struck off but show zero operational turnover. With the government’s 2026 AI-audit crackdown, we expect a massive “Culling of the Herd” where inactive companies will be forcibly liquidated to clean up the data.

Compliance-Induced Bankruptcy. It’s not the competition that kills Indian SMEs; it’s the paperwork. As the state moves toward real-time digital auditing, companies that haven’t digitized their back-end will spend more on “fixing errors” and “paying fines” than on R&D or marketing.