NEW DELHI, INDIA (IST)

00:00:00 PM

|

Loading...

DETECTING LOCATION...

00:00:00 PM

|

Loading...

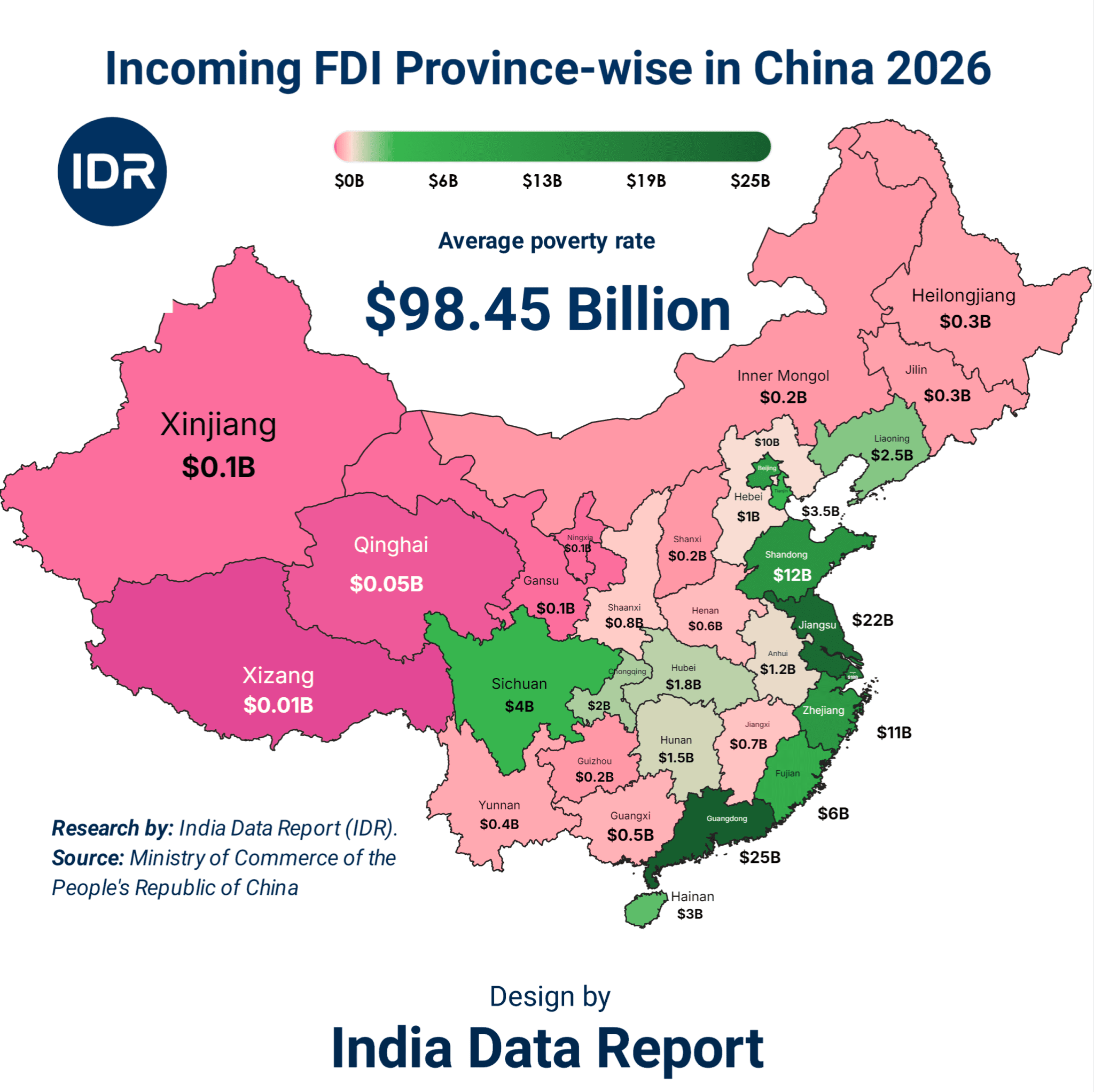

| Province | Incoming FDI (USD Billion) |

|---|---|

| Guangdong | $25.0B |

| Jiangsu | $22.0B |

| Zhejiang | $12.0B |

| Shandong | $11.0B |

| Fujian | $6.0B |

| Sichuan | $4.0B |

| Shanghai | $3.5B |

| Beijing | $2.5B |

| Tianjin | $2.0B |

| Hebei | $1.8B |

| Hubei | $1.8B |

| Hunan | $1.5B |

| Anhui | $1.2B |

| Henan | $1.0B |

| Liaoning | $0.8B |

| Jiangxi | $0.7B |

| Heilongjiang | $0.3B |

| Jilin | $0.3B |

| Inner Mongolia | $0.2B |

| Shanxi | $0.2B |

| Chongqing | $0.2B |

| Guangxi | $0.5B |

| Yunnan | $0.4B |

| Guizhou | $0.5B |

| Shaanxi | $0.6B |

| Gansu | $0.1B |

| Ningxia | $0.1B |

| Qinghai | $0.05B |

| Xinjiang | $0.1B |

| Xizang (Tibet) | $0.01B |

| Hainan | $3.0B |

The numbers coming out of Beijing aren’t just statistics; they are a desperate SOS signal masked as a balance sheet. While the Ministry of Commerce of the People’s Republic of China attempts to project a facade of stability with a total incoming Foreign Direct Investment (FDI) of $98.45 billion, any strategist worth their salt can see the rot beneath the foundation. We are witnessing the most significant tectonic shift in global capital since the 1990s. The “Factory of the World” is facing an existential identity crisis, and the money the cold, hard, unsentimental global capital is already halfway out the door.

For decades, the world operated on a simple, greedy premise: park your supply chain in China, ignore the geopolitical red flags, and reap the margins. That era died in the post-pandemic hangover. Today, China’s FDI landscape is a map of extreme inequality and systemic fragility. When you look at the $25 billion flowing into Guangdong versus the pathetic $10 million in Xizang (Tibet), you aren’t looking at “regional development.” You are looking at a country struggling to keep its coastal engines from seizing up while its interior remains an economic graveyard.

Let’s be blunt. $98.45 billion sounds like a massive number to the uninitiated. But for an economy the size of China, it’s a drop in the ocean compared to the capital flight and the massive debt bubbles in their property sector. Global investors are no longer asking “How much can I make in China?” They are asking “How fast can I get my principal out?”

The concentration of wealth is staggering. Look at the data. A handful of coastal provinces are doing the heavy lifting, while the rest of the country is essentially an economic spectator.

| Province | FDI (USD Billion) | Economic Character | Investment Risk Profile |

| Guangdong | $25.0B | Manufacturing & Tech Hub | High (Supply chain decoupling) |

| Jiangsu | $22.0B | High-end Industrial | Moderate (Export dependency) |

| Zhejiang | $12.0B | Private Enterprise/E-commerce | High (Regulatory crackdowns) |

| Shanghai | $3.5B | Financial Gateway | Extreme (Policy volatility) |

| Western Provinces (Avg) | < $0.5B | Resource Extraction | Low (Non-existent interest) |

The Bitter Truth: Over 60% of China’s FDI is trapped in just three coastal provinces. If the maritime trade routes in the South China Sea face even a minor kinetic tremor, $60 billion of annual investment vanishes overnight. China isn’t an economic monolith; it’s a coastal fringe supporting a hollow core.

Capital is a coward. It goes where it is protected and flees where it is threatened. The CCP’s recent obsession with “National Security” over “Economic Growth” has sent a clear message to Wall Street and the City of London: Your assets are our assets if we decide they are.

When you see Shanghai—the supposed crown jewel of Chinese finance—pulling in a measly $3.5 billion, you have to wonder what the “experts” are smoking. For a city of that scale, $3.5 billion isn’t an investment; it’s maintenance money. It means the big institutional players are no longer building new headquarters; they are just keeping the lights on while they scout locations in Vietnam, India, and Mexico.

The “China Plus One” strategy isn’t a theory anymore. It’s a boardroom mandate. The greed that once drove companies to Shenzhen has been replaced by a primal fear of being “trapped” behind a sudden bamboo curtain of sanctions or asset freezes.

The disparity between the East and West of China is a ticking social time bomb. The Ministry of Commerce lists Gansu at $0.1 billion and Qinghai at $0.05 billion. These aren’t just low numbers; they are zeros in the eyes of the global market.

Why does this matter to you? Because a country that cannot distribute its investment internally is a country that will eventually face internal collapse. The coastal provinces are getting richer (or at least holding steady), while the vast interior is being left to rot in a debt-fueled shadow. This is the “Middle Income Trap” on steroids.

| Region | Combined FDI | Population (Approx) | Per Capita FDI Impact |

| Top 3 (Guangdong, Jiangsu, Zhejiang) | $59.0B | ~250 Million | High / Growth-Sustaining |

| Bottom 10 (Gansu, Xinjiang, Tibet, etc.) | ~ $0.6B | ~150 Million | Negligible / Poverty Trap |

The Bitter Truth: Beijing’s “Go West” policy has been a catastrophic failure in attracting foreign capital. Global investors don’t care about political slogans; they care about logistics, and the logistics of inner China are a nightmare of bureaucracy and state control.

While China’s Ministry of Commerce puts out these “stable” figures, the India Data Report (IDR) suggests a different story. The flow is diverting. Investors are tired of the “black box” nature of Chinese accounting. In China, you don’t own a business; you lease it from the Party’s goodwill.

In contrast, the global shift toward democratic supply chains is real. It’s not that India or Vietnam are “perfect,” but they offer something China no longer can: Predictability. When a CEO in 2026 looks at their 2030 roadmap, they see China as a volatility risk. They see the $98 billion FDI not as a sign of strength, but as the final gasps of an era where China could dictate terms to the world.

We are currently living through a “Truth Crisis.” Is the $98.45 billion figure even real? In a system where data is a tool for propaganda, we must look at the psychological state of the investor. The “fear of missing out” (FOMO) that fueled the China boom from 2001 to 2018 has been replaced by the “fear of being caught” (FOBC).

The common man thinks their iPhone or their car parts are just “made in China.” But the strategist knows that those parts are the result of FDI decisions made five years ago. The new decisions—the ones being made today in 2026—are steering clear of the mainland. What we see today is the momentum of the past. The future is being written elsewhere.

| Sector | Current FDI Strength | Vulnerability Level (2026-2030) | Alternative Destinations |

| Semiconductors | High (Internal focus) | Extreme (Sanctions) | USA, India, Taiwan |

| Electric Vehicles | Moderate | High (EU/US Tariffs) | Mexico, Thailand, Germany |

| E-commerce/Tech | Declining | Very High (Regulation) | SE Asia, India |

| Heavy Machinery | Stable | Moderate | Vietnam, Indonesia |

A Golden Opportunity: For the rest of the world, China’s inward-turning policy is a gift. As China prioritizes state-owned enterprises (SOEs) over foreign players, the intellectual and financial capital is looking for a new home. Those who position themselves as the “stable alternative” will inherit the trillions.

What the Ministry of Commerce won’t tell you is how much of that $98 billion is “round-tripping” Chinese money sent to Hong Kong or the British Virgin Islands and then brought back to claim “foreign” tax incentives. Real, organic, Western-originating FDI is in a freefall.

The human element here is desperation. The Chinese middle class, once the primary target of foreign brands, is now saving every penny because they are terrified of the property market collapse. If the local consumer isn’t spending, why would a foreign firm invest in a new factory? The logic has broken down.

If you are waiting for a “return to normal” in China, you are going to go broke. The “Old Normal” is dead and buried.

By 2030, the FDI map of China will look even more lopsided. Guangdong and Jiangsu will likely maintain some level of investment due to their sheer scale, but the “service-based” FDI in Shanghai and Beijing will crater as multinational banks move their regional HQs to Singapore or Tokyo. China will transition into a “fortress economy”—self-sufficient but stagnant.

The dream of China as a unified global economic hegemon is fading. By 2047, the 100th anniversary of the PRC’s rivals’ rise, we will see a China that is a collection of high-tech coastal enclaves surrounded by a vast, aging, and underfunded hinterland. The FDI will be hyper-specific only in sectors where the world absolutely cannot find an alternative (like rare earth processing).

India is the primary beneficiary of this tectonic shift, but only if it can fix its own bureaucratic hurdles. The capital is ready to move; it just needs a landing pad that doesn’t feel like a trap.

To the CEOs, the Strategy Officers, and the Private Equity hawks: The data doesn’t lie, but the people who present it do. A total of $98.45 billion in a country of 1.4 billion people is not a success; it is a warning.

Audit Your Exposure: If 20% or more of your supply chain is tied to the top 5 Chinese provinces, you are one geopolitical “accident” away from bankruptcy.

Follow the Yield, Not the History: Don’t invest in China because “that’s where we’ve always been.” The delta of growth has shifted.

Watch the Interior: If FDI in Sichuan and Hubei doesn’t triple in the next three years, the Chinese domestic market is a dead end.

The Great Wall isn’t just a monument anymore; it’s a cage. The question is: are you on the outside looking in, or are you trapped inside with your capital?