NEW DELHI, INDIA (IST)

00:00:00 PM

|

Loading...

DETECTING LOCATION...

00:00:00 PM

|

Loading...

| Rank | State | Marriage Rate |

|---|---|---|

| 1 | Utah | 51.7% |

| 2 | Idaho | 45.2% |

| 3 | North Dakota | 42.8% |

| 4 | South Dakota | 41.5% |

| 5 | Nebraska | 40.3% |

| 6 | Wyoming | 38.9% |

| 7 | Oklahoma | 38.2% |

| 8 | Arkansas | 37.8% |

| 9 | Kansas | 37.4% |

| 10 | Iowa | 36.9% |

| 11 | Georgia | 36.1% |

| 12 | North Carolina | 35.7% |

| 13 | Virginia | 35.3% |

| 14 | Mississippi | 34.9% |

| 15 | Missouri | 34.1% |

| 16 | Texas | 33.7% |

| 17 | Alabama | 33.3% |

| 18 | South Carolina | 32.9% |

| 19 | Tennessee | 32.5% |

| 20 | Ohio | 32.1% |

| 21 | Montana | 31.7% |

| 22 | Arizona | 31.3% |

| 23 | Alaska | 30.5% |

| 24 | Nevada | 30.1% |

| 25 | Florida | 29.7% |

| 26 | Michigan | 28.9% |

| 27 | Pennsylvania | 28.5% |

| 28 | Minnesota | 28.1% |

| 29 | West Virginia | 27.6% |

| 30 | Wisconsin | 29.3% |

| 31 | Illinois | 27.3% |

| 32 | Washington | 26.9% |

| 33 | Oregon | 26.5% |

| 34 | Colorado | 26.1% |

| 35 | New York | 24.5% |

| 36 | Maine | 23.3% |

| 37 | California | 21.3% |

| 38 | Hawaii | 21.7% |

The American marriage market is not just cooling down; it is facing a structural collapse that will reshape western capitalism by 2030. For decades, Wall Street and mainstream sociologists looked at dipping nuptial rates as a mere cultural shift a lifestyle choice by millennials and Gen Z who prefer traveling or cohabitation over a piece of paper. They are dead wrong. This is an economic crisis masked as a social trend.

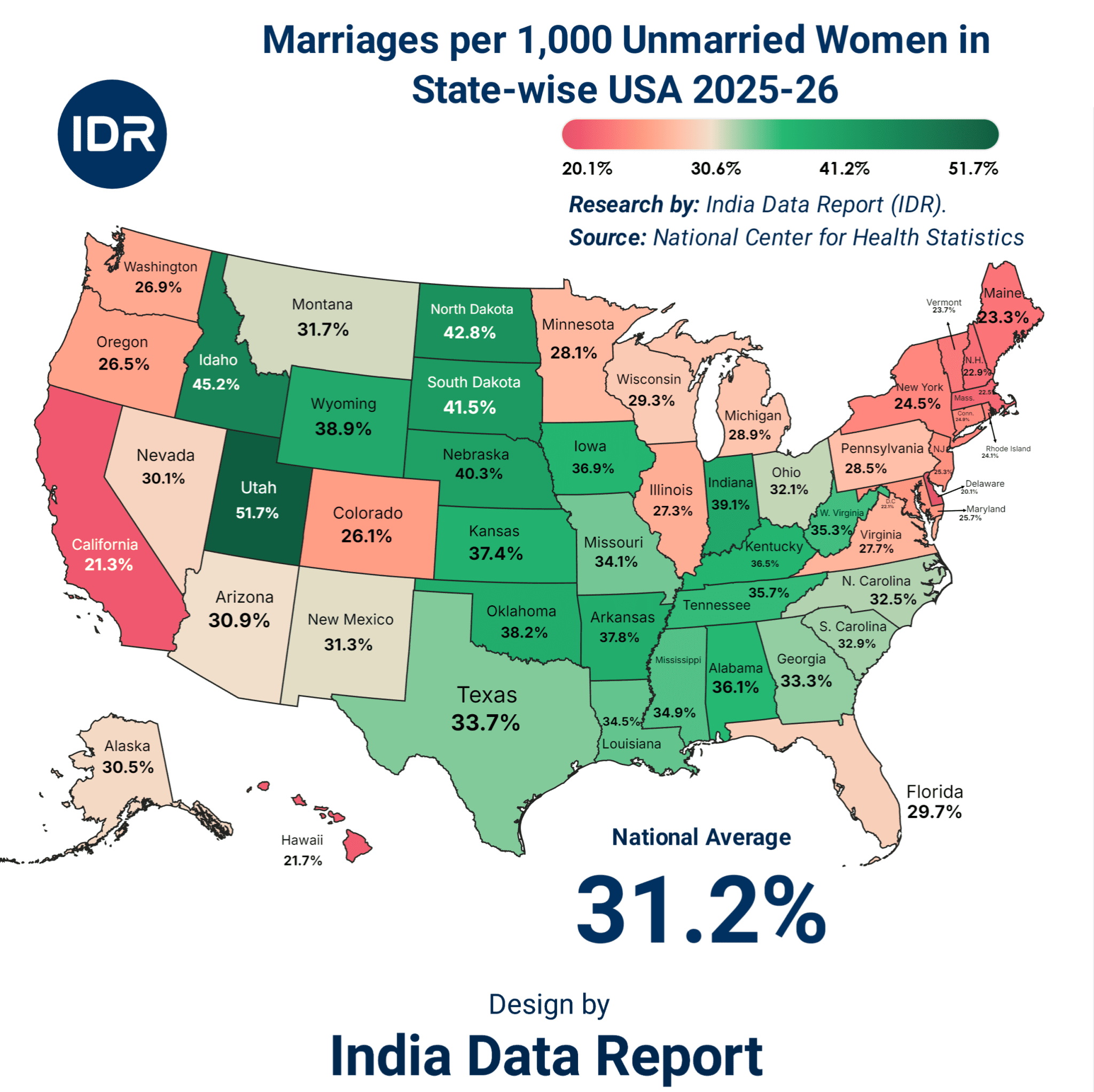

When you look at the raw data from 2025–2026, the numbers tell a story of regional survival versus coastal extinction. Marriage in America has transformed from a universal milestone into a luxury consumer good available only to those who can afford the financial premium of modern stability.

Let’s look at the absolute peak of this crumbling mountain before we dissect the valley below.

If you want to see where the old world still breathes, you have to look at the religious and agrarian corridors of the United States. Utah is currently sitting at the absolute top of the index with a 51.7% marriage rate per 1,000 unmarried women. Idaho follows at 45.2%, with North Dakota, South Dakota, and Nebraska rounding out the top five.

+------+--------------+---------------+

| Rank | State | Marriage Rate |

+------+--------------+---------------+

| 1 | Utah | 51.7% |

| 2 | Idaho | 45.2% |

| 3 | North Dakota | 42.8% |

| 4 | South Dakota | 41.5% |

| 5 | Nebraska | 40.3% |

+------+--------------+---------------+

The Bitter Truth: High marriage rates in these states are not driven by sudden economic superiority. They are fueled by cultural infrastructure and a lower baseline cost of living that permits young couples to take financial risks together. However, even these numbers are declining compared to the historical baseline of the early 2000s. The walls are closing in here too.

Why are these states holding the line? Look at the cost of entry. In Salt Lake City, Boise, or Bismarck, the ratio of median home price to median household income—while strained by recent inflation—still hovers within a realm of mathematical possibility for a dual-income couple in their mid-twenties. Combine that with deep-rooted religious institutions (the LDS church in Utah and Idaho, and traditional Lutheran/Catholic roots in the Dakotas) that actively subsidize the social cost of marriage, and you get a temporary firewall against the national trend.

But do not confuse survival with immunity. The economic engine driving these high numbers is under siege. As coastal capital migrates inward, driving up real estate values in places like Boise and Provo, the local population is being priced out of their own traditions. The “marriage premium”—the financial benefit of combining two incomes to build equity—is turning into a survival requirement rather than a building block of wealth.

Move down the ladder into the American South and Midwest, and the numbers reveal a disturbing equilibrium. These are the states where economic anxiety acts as a literal contraceptive against long-term commitment.

+------+----------------+---------------+

| Rank | State | Marriage Rate |

+------+----------------+---------------+

| 11 | Georgia | 36.1% |

| 12 | North Carolina | 35.7% |

| 13 | Virginia | 35.3% |

| 14 | Mississippi | 34.9% |

| 15 | Missouri | 34.1% |

| 16 | Texas | 33.7% |

| 17 | Alabama | 33.3% |

| 18 | South Carolina | 32.9% |

| 19 | Tennessee | 32.5% |

| 20 | Ohio | 32.1% |

+------+----------------+---------------+

The Bitter Truth: The American South and Rust Belt are trapped in an economic no-man’s-land. Wages are too stagnant to comfortably support a wedding and a mortgage, yet social pressures still stigmatize alternative arrangements. The result? A paralyzed demographic that delays marriage indefinitely while waiting for a financial stability that isn’t coming.

Look at Texas at 33.7% or Ohio at 32.1%. These aren’t just statistics; they are reflections of structural shifts. Texas, despite its massive economic growth and corporate relocations, suffers from a widening wealth gap. The young professionals moving to Austin or Dallas might have high salaries, but they also bring massive student debt loads and a hyper-individualistic consumer mindset. Meanwhile, the native working class is dealing with soaring property taxes and rental costs that make the financial liability of a legal marriage look like madness.

In the Rust Belt, the story is older and darker. When factory gates slammed shut thirty years ago, they didn’t just take jobs—they destroyed the male breadwinner model that traditional American marriage was built upon. Today, with the rise of the gig economy and service-sector employment, the economic incentives to legally bind fortunes have flipped. Men without stable career trajectories are viewed as financial liabilities rather than partners, while women increasingly realize that a legal union in a low-growth economy can mean taking on someone else’s debt and risk without any corresponding upside.

Now let’s look at the bottom of the barrel, the engine rooms of modern global culture and finance: California (21.3%) and New York (24.5%). The narrative we are fed by Hollywood and the corporate press is that these states are hubs of progressive enlightenment where people simply choose to self-actualize through their careers rather than outdated domestic rituals.

What utter nonsense.

+------+------------+---------------+

| Rank | State | Marriage Rate |

+------+------------+---------------+

| 34 | Colorado | 26.1% |

| 35 | New York | 24.5% |

| 36 | Maine | 23.3% |

| 37 | California | 21.3% |

| 38 | Hawaii | 21.7% |

+------+------------+---------------+

The Bitter Truth: The coastal elite states have engineered a hyper-expensive reality where marriage has been effectively banned for anyone earning less than six figures. The absolute collapse of the nuptial rate in California and New York is the direct consequence of artificial housing scarcity, crushing taxation, and an atomized labor market that views human relationships as friction.

Let’s do the cold math on a young couple in Los Angeles or Brooklyn. The median home price in California hovers around $800,000. For two individuals earning average salaries, saving for a 20% down payment while paying premium rents and servicing student loans is a decades-long endeavor. A wedding which now averages over $35,000 nationally and easily double that in major metros—is a competing capital expenditure.

When facing a choice between a down payment on a 700-square-foot condo or an elegant party for one hundred people to satisfy family vanity, the rational consumer chooses neither. They stay single, lease an apartment they can barely afford, and channel their emotional energy into hyper-curated social media profiles and food delivery apps.

This is a psychological prison built by economic design. The fear of financial ruin outpaces the desire for companionship. In a high-risk, high-cost environment, a legal contract that exposes 50% of your future assets to asset division isn’t viewed as a sacrament it’s viewed as a terrible short position on your own career.

What happens to an economy when the basic building block of society the multi-generational, wealth-pooling household is dismantled? We are about to find out over the next four years. The traditional American economy was built on the assumption of domestic continuity. The housing market, the insurance industry, consumer credit, and retail sectors all depend on couples setting up homes, buying appliances, upgrading vehicles, and investing in children.

+--------------------------+----------------------------+----------------------------+

| Economic Sector | Historical Dynamic (Pairs) | Modern Reality (Singles) |

+--------------------------+----------------------------+----------------------------+

| Housing & Real Estate | Single family suburban | Studio rentals / Co-living |

| Consumer Discretionary | High-volume appliance buys | Micro-purchases / Subscriptions |

| Wealth & Asset Mgmt | Multi-generational trusts | Individual brokerage accounts |

| Healthcare & Insurance | Family plan optimization | Individual high-deductible |

+--------------------------+----------------------------+----------------------------+

The Golden Opportunity: Savvy capital allocators are aggressively pivoting away from family-centric goods toward single-serve infrastructure. Real estate investment trusts (REITs) are moving out of suburban developments and pouring billions into high-density single-occupancy rentals with built-in social amenities. If people cannot buy a family, you sell them a community via a monthly subscription.

This shift creates a massive wealth polarization. When two high earners marry in Utah or Idaho, they create a compounding wealth machine. They pool capital, lower their per-capita living expenses, maximize tax deductions, and purchase appreciating assets early.

When two individuals remain single in California or New York, they pay double the rent, lose tax advantages, and funnel their discretionary cash into depreciating consumer goods and experience-based services. The wealth gap of the future will not just be between the rich and the poor; it will be between the coupled and the isolated.

The data from 2025–2026 is not a temporary statistical blip; it is the structural floor of a new economic paradigm. By 2030, the national average marriage rate will drop another 15%, stabilized only by a few regional holdouts that refuse to abandon their cultural infrastructure.

Here are three brutal predictions for the final years of this decade:

The American dream used to include a white picket fence and a spouse. Today, the fence has been sold for scrap metal, and the spouse has been replaced by a lifestyle brand. If you are operating a business or managing capital based on the old playbook of American family dynamics, you are investing in a ghost town. Look at the numbers, accept the reality, and position your portfolio for an isolated world.