NEW DELHI, INDIA (IST)

00:00:00 PM

|

Loading...

DETECTING LOCATION...

00:00:00 PM

|

Loading...

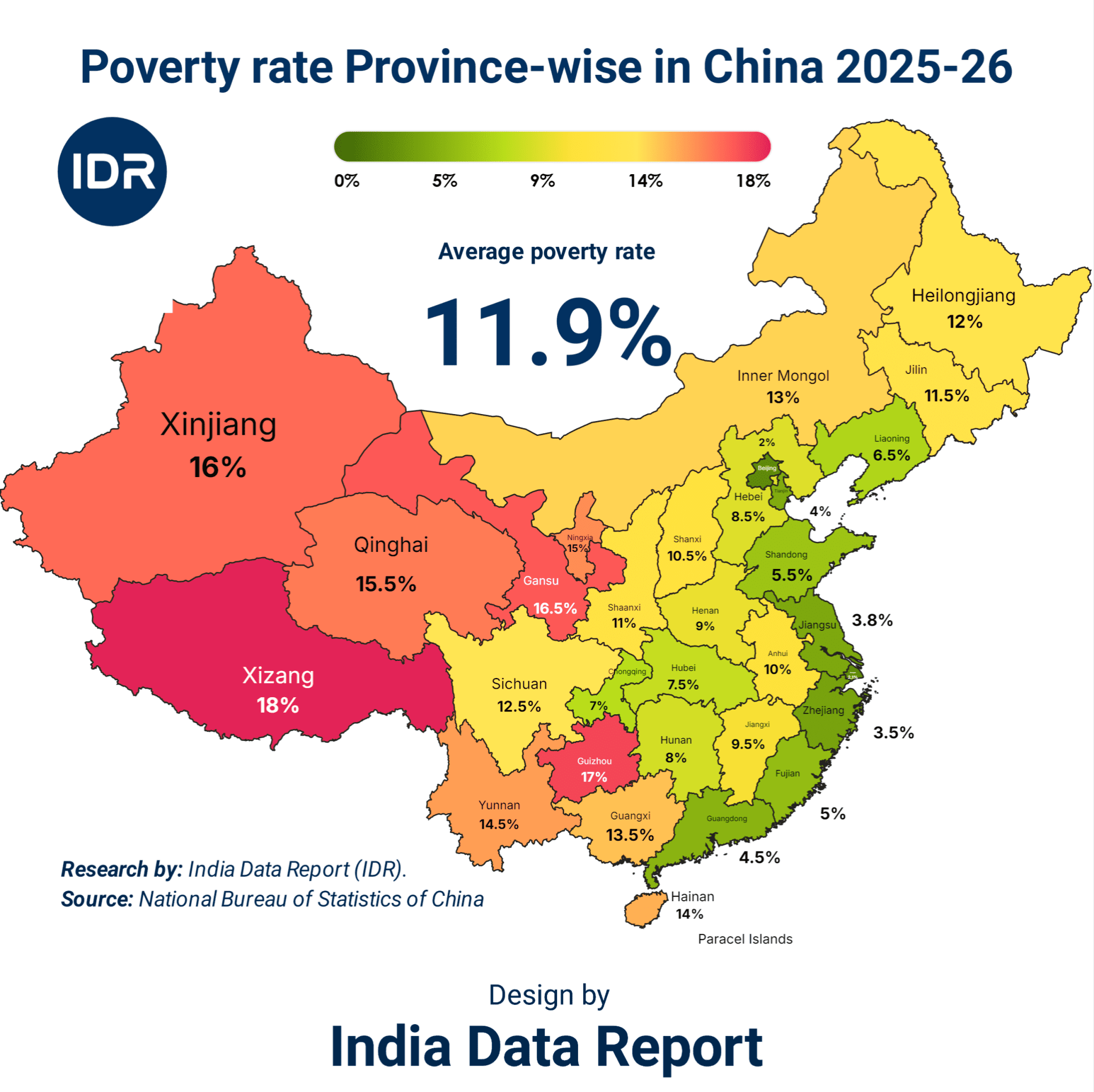

| Rank | Province | Poverty Rate (%) |

|---|---|---|

| 1 | Xizang (Tibet) | 18.0% |

| 2 | Guizhou | 17.0% |

| 3 | Gansu | 16.5% |

| 4 | Xinjiang | 16.0% |

| 5 | Qinghai | 15.5% |

| 6 | Yunnan | 14.5% |

| 7 | Hainan | 14.0% |

| 8 | Guangxi | 13.5% |

| 9 | Inner Mongolia | 13.0% |

| 10 | Sichuan | 12.5% |

| 11 | Heilongjiang | 12.0% |

| 12 | Jilin | 11.5% |

| 13 | Shanxi | 11.0% |

| 14 | Shaanxi | 10.5% |

| 15 | Hubei | 10.0% |

| 16 | Hunan | 9.5% |

| 17 | Chongqing | 9.0% |

| 18 | Henan | 8.5% |

| 19 | Jiangxi | 8.0% |

| 20 | Anhui | 7.5% |

| 21 | Hebei | 7.0% |

| 22 | Liaoning | 6.5% |

| 23 | Shandong | 5.5% |

| 24 | Fujian | 5.0% |

| 25 | Guangdong | 4.5% |

| 26 | Tianjin | 4.0% |

| 27 | Jiangsu | 3.8% |

| 28 | Zhejiang | 3.5% |

| 29 | Shanghai | 3.5% |

| 30 | Beijing | 3.0% |

The official narrative coming out of Beijing has been rehearsed to perfection: absolute poverty has been eradicated, the system has triumphed, and wealth is flowing seamlessly across the dragon’s empire. But economics is an unforgiving science. It does not care about political choreography or grand national addresses. When you look past the neon-lit skyscrapers of Shanghai and the artificial intelligence hubs of Shenzhen, a far more dangerous reality emerges.

China is not operating as a unified economic superpower. It is running a dual-engine system where one half of the country enjoys First-World luxury while the other half is quietly trapped in a cycle of structural deprivation. The local idiom says, “The sky is high and the emperor is far away” (山高皇帝远). Today, that distance is measured not just in kilometers, but in a staggering chasm of disposable income, opportunity, and survival.

The numbers for 2025–2026 expose a truth that state media prefers to bury under infrastructure statistics. We are witnessing an internal economic apartheid. While coastal elites debate luxury real estate trends, the western and interior frontiers are battling a silent, grinding crisis. This isn’t just a bump in the road toward common prosperity; it is a structural fault line that threatens the very core of the world’s second-largest economy.

For decades, global markets swallowed the story of the homogeneous Chinese miracle. Foreign investors treated the entire territory as a monolithic consumption engine. That was a critical mistake. The reality is a deeply fragmented landscape where economic geography dictates human destiny.

If you are born in Beijing or Shanghai, you belong to a society with a poverty rate hovering between 3.0% and 3.5%. You have access to world-class healthcare, premium capital, and global supply chains. But travel west toward Xizang (Tibet) or Guizhou, and the economic fabric shreds apart completely, revealing poverty rates as high as 17% to 18%.

This is not a accidental gap; it is a structural feature of an export-heavy, coastal-centric growth model that has left the hinterlands behind. The state spent trillions on high-speed rail lines and empty apartment complexes in the interior to artificially boost provincial GDP figures. Yet, the human capital in these regions remains disconnected from the wealth generation machine. You cannot eat concrete, and you cannot pay for modern healthcare with a six-lane highway that leads to a ghost town.

The hard data from the 2025–2026 provincial audit shatters the myth of equal distribution. The average provincial poverty rate sits at 11.9%. But averages are the ultimate statistical camouflage. They blend the hyper-wealthy with the desperate to present a comfortable lie. When we uncouple the regions, the sheer scale of internal disparity becomes impossible to ignore.

| Rank | Province | Poverty Rate (%) | Economic Character |

| 1 | Xizang (Tibet) | 18.0% | Frontier / Subsidized |

| 2 | Guizhou | 17.0% | Interior / Heavy Debt |

| 3 | Gansu | 16.5% | Arid / Industrial Legacy |

| 4 | Xinjiang | 16.0% | Border / Resource Intensive |

| 5 | Qinghai | 15.5% | High-Altitude / Isolated |

| 6 | Yunnan | 14.5% | Agricultural Border |

| 7 | Hainan | 14.0% | Tourism Depended / Enclave |

| 8 | Guangxi | 13.5% | Southern Interior |

| 9 | Inner Mongolia | 13.0% | Resource Dependent |

| 10 | Sichuan | 12.5% | Megacity Hub with Poor Periphery |

The Bitter Truth: The western provinces are functioning as economic colonies for the coast—providing cheap raw materials, electricity, and migrant labor while retaining almost none of the high-value wealth generated by the final products.

To truly understand the psychological strain on the average citizen, look at the bottom of the table. The concentration of wealth along China’s coastline has created a series of economic fortresses that are completely detached from the struggles of the rest of the country.

| Rank | Province | Poverty Rate (%) | Integration Level |

| 26 | Tianjin | 4.0% | Global Port Hub |

| 27 | Jiangsu | 3.8% | High-Tech Manufacturing |

| 28 | Zhejiang | 3.5% | Private Enterprise Capital |

| 29 | Shanghai | 3.5% | Global Financial Nexus |

| 30 | Beijing | 3.0% | Political & Capital Core |

The Golden Opportunity: For multinational corporations and premium brands, the “China Market” does not exist. The only predictable, resilient consumer base is concentrated within these five coastal fortresses and Guangdong. Marketing outside this zone is an exercise in diminishing returns.

The distance between Beijing’s 3.0% poverty rate and Tibet’s 18.0% is a six-fold increase in economic vulnerability. In any Western democracy, a regional disparity of this magnitude would trigger massive political gridlock and policy overhauls. In China, it is managed through narrative control and internal migration restrictions like the Hukou system.

The Hukou (household registration) acts as an invisible border control within the country. A migrant worker from Guizhou working on a construction site in Shanghai cannot access free public education for their children or subsidized healthcare in the city. They are treated as second-class citizens within their own nation. This ensures that wealth generated in Shanghai stays in Shanghai, while the social costs of poverty are exported back to the interior provinces.

Between the hyper-wealthy coast and the impoverished western borders lies the industrial and agricultural spine of China. These mid-tier provinces are the most vulnerable to the current global shift in supply chains. As multinational companies adopt “China Plus One” strategies, moving factories to Vietnam, India, or Mexico, these regions are losing their primary economic lifeline.

| Rank | Province | Poverty Rate (%) | Vulnerability Drivers |

| 11 | Heilongjiang | 12.0% | Rust Belt / Aging Population |

| 12 | Jilin | 11.5% | Heavy Industrial Decline |

| 13 | Shanxi | 11.0% | Coal Dependency / Carbon Taxes |

| 14 | Shaanxi | 10.5% | Real Estate Over-reliance |

| 15 | Hubei | 10.0% | Manufacturing Slowdown |

| 16 | Hunan | 9.5% | Agricultural Margin Squeeze |

| 17 | Chongqing | 9.0% | Infrastructure Debt |

| 18 | Henan | 8.5% | Agrarian Overpopulation |

| 19 | Jiangxi | 8.0% | Brain Drain to Coast |

| 20 | Anhui | 7.5% | Supply Chain Spillover Dependent |

The Bitter Truth: The Rust Belt provinces of Northeast China (Heilongjiang and Jilin) are facing an demographic cliff. The young, capable workforce has fled to the coast, leaving behind an aging population and bankrupt local government pension funds that rely entirely on central government bailouts.

Consider the human cost in a province like Henan (8.5% poverty) or Shanxi (11.0%). These are regions that built the raw materials for China’s infrastructure boom. They mined the coal, smelted the steel, and provided the hands that laid the asphalt. Now, with the real estate bubble burst and local governments drowning in debt from the Shadow Banking crisis, these provinces are staring into an economic abyss.

The central government’s crackdowns on tech, tutoring, and real estate sectors over the past few years have systematically wiped out the entry-level corporate jobs that bright graduates from these middle provinces relied on to escape the cycle. Today, the youth unemployment rate remains dangerously high, creating a class of over-educated, under-employed citizens who are “lying flat” (Tang Ping) because they realize the game is rigged against them.

The legitimacy of the political establishment has rested on a single unwritten contract since the days of Deng Xiaoping: Give up your political voice, and in return, you will get richer every year. For thirty years, that contract held up. Wealth was growing fast enough that even if your neighbor got rich faster, your own standard of living was visibly improving.

That contract is now expiring. When growth slows down to real, unpadded figures, inequality stops being a statistical annoyance and becomes an existential threat. Fear is replacing greed as the primary driver of economic behavior in China.

This psychological shift changes everything. When a population acts out of fear rather than optimism, they stop spending. They hoard cash in state banks, they avoid long-term investments, and they refuse to have children. China’s current demographic collapse—the fastest peacetime population decline in modern history—is the direct result of this economic anxiety. Raising a child in a system where only the top 10% in coastal enclaves succeed is a financial gamble most families can no longer afford.

To visualize the sheer polarization of the Chinese economy, let us look at the absolute extremes. When you look at the top five highest-poverty provinces versus the top five lowest-poverty provinces, you are looking at two entirely different nations occupying the same geographic space.

| Highest Poverty Provinces | Rate (%) | Lowest Poverty Provinces | Rate (%) |

| Xizang (Tibet) | 18.0% | Beijing | 3.0% |

| Guizhou | 17.0% | Shanghai | 3.5% |

| Gansu | 16.5% | Zhejiang | 3.5% |

| Xinjiang | 16.0% | Jiangsu | 3.8% |

| Qinghai | 15.5% | Tianjin | 4.0% |

The Bitter Truth: The combined population of the high-poverty interior zones runs into hundreds of millions of people. This means that despite having an economy that rivals the United States in nominal GDP, China has a domestic market capacity that is severely restricted because a massive portion of its population is priced out of modern consumerism.

This polarization means that policy solutions designed in Beijing are often completely decoupled from the needs of the provinces. When the central bank cuts interest rates to stimulate the economy, the liquidity doesn’t flow to small businesses in Qinghai or agricultural cooperatives in Yunnan. It flows directly into the financial ecosystem of Shanghai and Shenzhen, inflating asset bubbles rather than creating real jobs where they are needed most.

Let us drop the diplomatic phrasing and look at what the next four years actually hold for the Chinese economic model. The current trajectory is unsustainable. Beijing cannot continue to subsidize the interior through debt-fueled infrastructure while the coast hoards the high-value returns of global trade.

No amount of official rhetoric can alter the math. The provincial poverty rates of 2025–2026 show that the foundations of China’s economic rise are unevenly laid. A house built on two different foundations cannot stand indefinitely when the storm hits.

For international strategists, businesses, and investors, the lesson is clear: do not look at China through the lens of national averages. The real story is written in the contrast between the wealth of the coast and the struggles of the interior. If you fail to map your strategy to this fractured reality, you are investing in an illusion that is rapidly fading away.