NEW DELHI, INDIA (IST)

00:00:00 PM

|

Loading...

DETECTING LOCATION...

00:00:00 PM

|

Loading...

The world is looking at the wrong numbers. For decades, Wall Street, Washington, and global boardrooms have treated China as a monolithic economic behemoth, reacting with panic or praise whenever Beijing releases its national aggregate GDP. But national aggregates are a lie. They are a statistical smoke screen designed to project uniform, unstoppable strength.

If you want to know where the global economy is actually heading, you have to look under the hood. You have to look at the provinces.

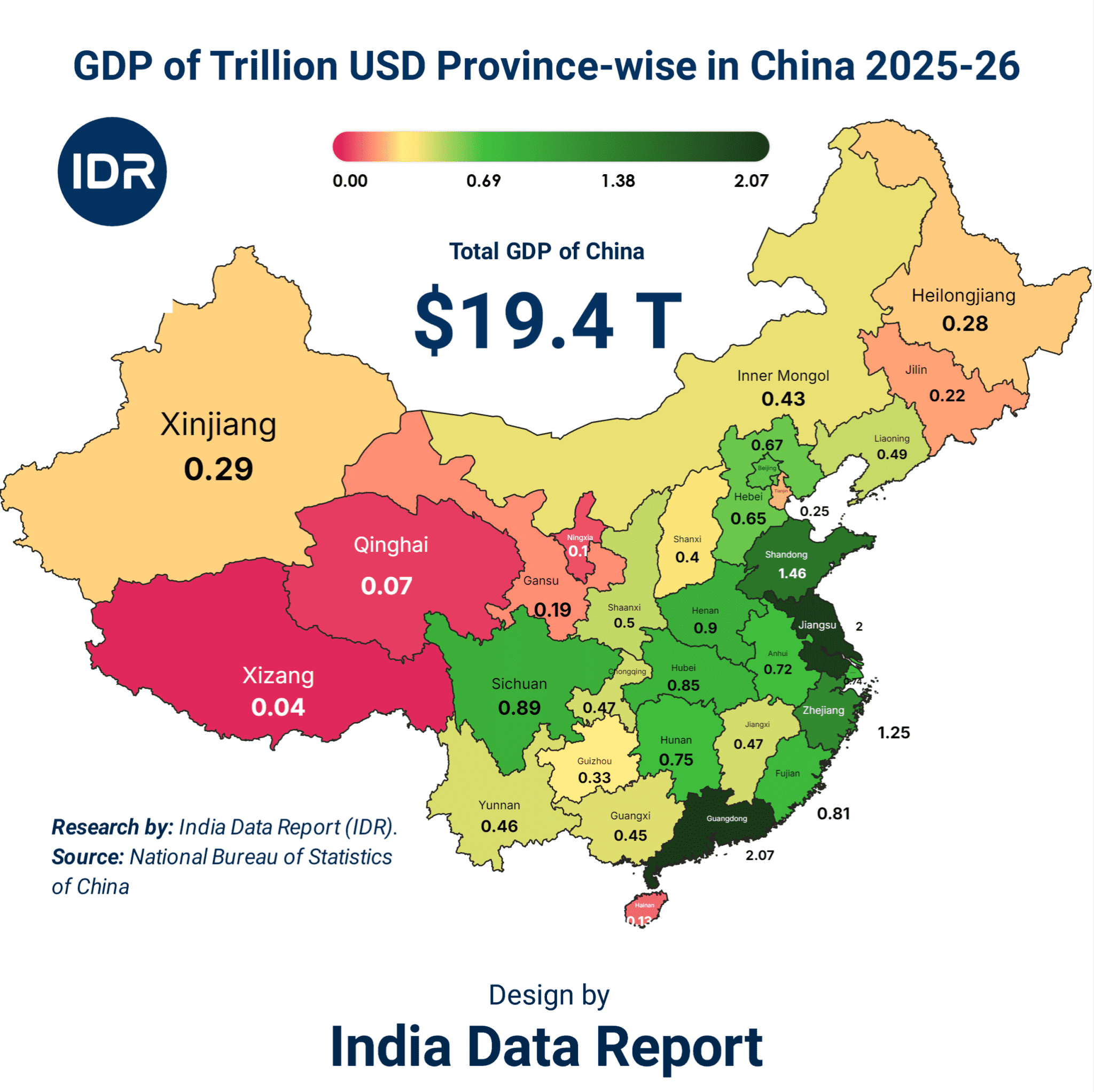

When you dissect the actual provincial output for 2025–26, a terrifying and fascinating reality emerges. A single Chinese province, Guangdong, is now generating $2.07 trillion in economic output. To put that in perspective, if Guangdong were an independent nation, its economy would comfortably outrank major global G20 nations like Australia, South Korea, and Spain.

What the data actually reveals is an economy radically out of balance, a country fractured into hyper-industrialized coastal empires and desperate, debt-ridden internal territories. Beijing has built a shimmering, high-tech facade on the coast, but the foundation in the hinterlands is cracking. We are witnessing the limits of state-capitalism, where the fear of social unrest drives reckless regional investments, and the greed of local bureaucrats has created a ghost-town economy.

Let’s strip away the propaganda and look at the hard truth of who actually holds the wealth in China, and what it means for your investments, your business, and the global balance of power as we march toward 2030.

The sheer disparity between China’s top-performing regions and its economic basement is staggering. The wealth of the nation is heavily concentrated in a tiny cluster of coastal powerhouses. These provinces have sucked the oxygen out of the rest of the country, attracting the majority of foreign direct investment, the brightest minds, and the most advanced manufacturing supply chains.

Take a look at the actual distribution of power across the top ten economic engines driving the Chinese machine.

| Rank | Province | GDP (Trillion USD) | Primary Economic Driver |

| 1 | Guangdong | 2.07 | Tech, Advanced Manufacturing, Global Export |

| 2 | Jiangsu | 1.46 | Electronics, Chemicals, Heavy Industrial Tech |

| 3 | Shandong | 1.25 | Agriculture, Energy, Machinery Manufacturing |

| 4 | Zhejiang | 1.20 | E-commerce, Private Enterprise, Light Industry |

| 5 | Sichuan | 0.89 | Domestic Consumption, Hydropower, Tech Hubs |

| 6 | Henan | 0.85 | Agriculture, Logistics, Raw Materials |

| 7 | Fujian | 0.81 | Shipping, Apparel, Battery Technology |

| 8 | Hubei | 0.75 | Automotive Manufacturing, Transport Logistics |

| 9 | Hunan | 0.72 | Heavy Machinery, Metallurgical Industries |

| 10 | Hebei | 0.67 | Steel Production, Heavy Industry, Energy |

Kadhwa Sach (The Bitter Truth): The combined GDP of just the top four provinces (Guangdong, Jiangsu, Shandong, and Zhejiang) totals a massive $5.98 trillion. This represents nearly a third of the entire nation’s economic output. The remaining dozens of provinces are effectively economic colonies, feeding raw materials and cheap labor into these four coastal monsters while drowning in their own localized debt.

If you are a global supply chain manager, you aren’t dealing with “China.” You are dealing with Guangdong and Jiangsu. Guangdong alone, with its tech hubs in Shenzhen and manufacturing lines in Dongguan, acts as the central nervous system of global consumer electronics.

But this extreme concentration introduces a massive point of failure. When a supply chain bottleneck, a geopolitical sanction, or a localized energy crisis hits Guangdong, it doesn’t just impact China—it paralyzes the world. The old saying goes, “When the wind blows, the grass bends.” But when Guangdong sneezes, the global tech sector catches double pneumonia.

Move just a step below the absolute elite, and you encounter the mid-tier provinces and the politically heavy mega-cities. This is where the narrative of seamless, unlimited growth begins to fall apart. Look at the numbers for the industrial heartlands and the political crown jewels like Beijing and Shanghai.

| Rank | Province / Municipality | GDP (Trillion USD) | Economic Realities & Vulnerabilities |

| 11 | Anhui | 0.65 | Rising tech hub, but heavily dependent on Yangtze spillover. |

| 12 | Beijing | 0.49 | State-Owned Enterprise (SOE) heavy, highly regulatory. |

| 13 | Shanghai | 0.49 | Financial capital, highly vulnerable to global capital flight. |

| 14 | Liaoning | 0.47 | Part of the aging “Rust Belt,” struggling with legacy industrial debt. |

| 15 | Shaanxi | 0.47 | Energy-dependent, highly vulnerable to green transition shifts. |

| 16 | Chongqing | 0.45 | Massive infrastructure buildout, running on high local debt. |

| 17 | Inner Mongolia | 0.43 | Coal and mining-dominated, volatile commodity-reliant economy. |

| 18 | Jiangxi | 0.40 | Traditional manufacturing, squeezed by coastal competition. |

| 19 | Yunnan | 0.46 | Tourism and agriculture, low tech-adoption rates. |

| 20 | Guangxi | 0.40 | Trade gateway to ASEAN, but low internal consumption. |

Sunera Avsar (The Golden Opportunity): For international investors looking to diversify away from the hyper-competitive and politically scrutinized coastal hubs, the Anhui-Chongqing corridor offers a sweet spot. These regions are hungry for foreign capital, possess highly skilled labor at lower wage pressures, and are heavily backed by Beijing’s internal development subsidies.

Look closely at Shanghai and Beijing, sitting at $0.49 trillion each. For cities of their global stature, these numbers show a distinct flattening of growth. The reality on the ground is that the regulatory crackdowns on tech and finance over the past few years have taken a heavy toll.

The human element here is palpable. Walk through the financial districts of Pudong in Shanghai, and you no longer see the unbridled optimism of the 2010s. Instead, there is a palpable sense of anxiety. Young professionals, once eager to conquer the corporate world, are embracing the “lying flat” philosophy. They see the sky-high cost of living, the diminishing returns on their labor, and the tightening grip of state surveillance. The economic engine is running, but the drivers are exhausted.

Now, let’s look at what Beijing doesn’t want highlighted on the international stage: the deep periphery. The provinces that are structurally incapable of matching the growth of the coast, yet are forced to live under the same national monetary and political framework.

| Rank | Province / Territory | GDP (Trillion USD) | Structural Bottlenecks |

| 21 | Tianjin | 0.25 | Overtaken by neighboring ports, massive local corporate defaults. |

| 22 | Xinjiang | 0.29 | Geopolitically sensitive, heavily subsidized, trade barriers. |

| 23 | Heilongjiang | 0.28 | Severe demographic decline, youth out-migration, obsolete industry. |

| 24 | Jilin | 0.22 | Border-zone economic stagnation, heavy reliance on state bailouts. |

| 25 | Gansu | 0.19 | Arid terrain, low industrial base, trapped in poverty cycles. |

| 26 | Guizhou | 0.33 | High infrastructure spending that failed to generate real ROI. |

| 27 | Shanxi | 0.40 | Over-reliant on coal, facing immense structural transition pain. |

| 28 | Hainan | 0.17 | Free Trade Port experiment, yet to match HK or Singapore standard. |

| 29 | Ningxia | 0.10 | Small population, geographically isolated, resource-constrained. |

| 30 | Qinghai | 0.07 | Ecological buffer zone, virtually no industrial scale. |

| 31 | Xizang (Tibet) | 0.04 | Geopolitically isolated, entirely dependent on Beijing’s fiscal transfers. |

Kadhwa Sach (The Bitter Truth): Xizang, Qinghai, and Ningxia combined do not even equal 10% of Guangdong’s economic output. This is not a unified national economy; it is an empire of economic inequality. The inhabitants of these lower-tier provinces face radically different life trajectories, limited job prospects, and a severe lack of capital, creating a ticking demographic and social time bomb for the central government.

Consider Guizhou ($0.33 trillion). A few years ago, it was heralded as China’s big data mountain hub. The government poured billions into tunnels, bridges, and massive data centers.

But if you build a highway to nowhere, you don’t get economic velocity—you just get debt. Today, Guizhou is a stark example of the Local Government Financing Vehicle (LGFV) crisis. The roads are empty, the data centers are underutilized, and the local banks are functionally insolvent, kept alive only by accounting tricks and the sheer willpower of the People’s Bank of China.

To understand where this leaves us, we have to look past the spreadsheets and look at human psychology. Economics is ultimately nothing more than human behavior quantified. And right now, the dominant emotion across the Chinese provinces is fear.

For thirty years, the social contract in China was simple: give up your political voice in exchange for guaranteed economic upward mobility. Every year, your life would get better, your property value would rise, and your children would get richer.

The real estate crash has wiped out up to 70% of average household wealth, which was heavily concentrated in unfinished or depreciating concrete apartments in third- and fourth-tier provinces. When an individual’s primary asset loses value, they don’t spend; they hoard cash. This explains the deflationary spiral haunting the Chinese economy.

Beijing can inject liquidity into factories and boost industrial production all it wants, but they cannot force a terrified consumer in Henan or Gansu to buy a new car when they are worried about keeping their job tomorrow. The state is pushing on a string. They are manufacturing goods that neither their own people nor a increasingly protectionist Western market can absorb.

The current provincial trajectory is completely unsustainable. Between now and 2030, the illusion of uniform Chinese growth will shatter, replaced by a stark, bifurcated reality. Here are my definitive, data-backed strategic predictions for the remainder of this decade:

The writing is on the wall. The era of easy, unbridled Chinese growth is over. The numbers don’t lie, even if the central planning offices try to smooth them out. Investors, policymakers, and corporate leaders must stop analyzing China through a telescope and start looking through a microscope. Focus on the provinces, understand the deep internal fractures, and protect your capital accordingly.